Pix: everything you need to know about this payment method

02/11/2020Understand what pix is, how it came up and what is its impact in the future Brazilian payment market.

How do you make your payments? Still spending money with interbank fees? Do you waste time waiting for the money to be credited to your account? Since November 2020, Brazilians may resort to a more convenient, modern and economic option. It is Pix, a new electronic payment means developed by the Central Bank of Brazil.

It was conceived with the expectation of making great changes in the digital payment market in the country, which transacted nearly R$ 2 trillion in 2019, according to BBC Brazil. Two days after launching, more than 10 million Brazilians registered their identification keys. Find out about the reason for such success.

In this article we will answer the main questions about the Pix. Continue to read and find out why you need to adhere to this new payment method.

What is Pix?

Pix incorporates a series of innovation, to digitize, remove red tape and give dynamics to the wire transfer and payment market. The system promotes a direct transaction of amounts between accounts held by persons and/or companies, decreasing the number of intermediaries and operating costs. It is possible, for instance, to make a pix between different banks without paying any fee for this. It works 24/7, and completes the transaction within 10 seconds. Another essential change is the adoption of identification keys for each account, using people’s regular information (mobile phone number, social number, email, etc.) To make a transaction, the payer just needs to identify the beneficiary through the key and confirm the transaction.

The Pix Project was born on December 21, 2018, through the introduction of the Instant Payment System (SPI), mentioned in an internal communication of the Central Bank. This is the largest leap towards the Brazilian market’s digitization. Pix encourages financial inclusion of the population and match the country with the global initiatives to the same effect. The European Union, for instance, developed t he Single Euro Payments Area (SEPA), an instant credit transfer system among its member States. According to InfoMoney, there are around 50 countries throughout the world with systems similar to Pix. The Cointelegraph also points out the possibility of cryptocurrency companies to enter Brazil’s Financial System.

How Pix works

Consumers and companies may adhere to the new system by registering identification keys, as if they were a nickname for their accounts, made by the financial or payment institutions. Up to 5 keys per account per person and up to 20 keys per company may be used. It is possible to have Pix in more than one bank. What cannot be done is to repeat keys for different accounts. As the transfer is driven by this unique “nickname”, the amount is credited to the account corresponding to the informed key. Thus, you can have different keys for different accounts.

This peculiar aspect of the system entailed a rush for registration among financial and payment institutions, as there is a limitation of four possible items to be used as key: CPF/CNPJ, mobile phone number, email address or creation of a random number.

By February 2021, the Central Bank had registered more than 180 million keys, which shows that this payment method is making its way among Brazilians.

How to use Pix

To be registered in Pix, a bank account of any type is needed: checking, savings, or payment account. The users will inform the key they intend to use through internet banking or payment platform. This resource allows a faster identification of the delivery address of the amount.

However, to use Pix the key does not need to be registered. It is possible to make and receive payments without it, by informing the bank account data to those wishing to make a transfer through Pix or selecting this option instead of using a DOC or TED when making a transfer.

Is Pix secure?

Pix entails more visibility in the transactions and allows end to end traceability. The transfers are made and certified at the Brazilian Financial System Network (RSFN), a data communication system among financial institutions managed by the Central Bank. All information is protected by Bank Secrecy Law (Supplementary Law no. 105/2001) and Brazilian General Data Protection Law (Law no.13.709/2018).

Likewise all other financial transactions, financial and payment institutions are liable for frauds. These institutions must implement risk mitigation systems, anti-fraud barriers and limits of value for transfers. As transactions are “instantaneous”, there is no cancellation of transfers and the refund protocols are unclear. Thus, the Central Bank of Brazil – BCB allows the institutions to withhold the transaction for up to 1 hour in case of suspected fraud.

Does Pix have a cost?

According to the Central Bank, Pix cost is expected to be R$ 0.01 for each 10 transfers. Thus, the Free Pix was formalized for people, except in cases of receipt for sales of products or services. For companies, the financial or payment institution may charge a fee for use. However, the BCB stresses that the amounts will be much lower than those currently charged. Further to the low adhesion cost, other incentives for adoption of the new system by the trade are: the immediate availability of the funds, easy automation and checkout.

The future of payments

The promise of the new Pix is to promote a great change in the payment methods, comprising financial institutions and the entire consumer world. In the transfer scenario, the DOC (Money Order Document) and TED (Wire Transfer of Available Funds) trend to lose ground. By simplifying day-to-day transactions, Pix must replace the bank slips, debit cards and cash, for example.

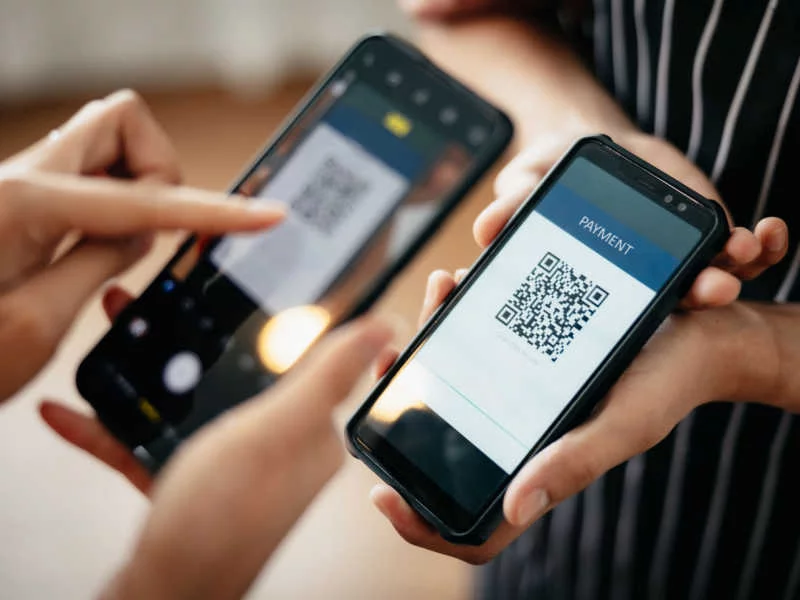

The Points of Sale (POS) terminals, known in Brazil as “little card machines”, also will feel the negative impacts of the novelty. Pix is compatible with contactless payment technology, as the near-field communication (NFC). They identification keys may be converted into static or dynamic QR codes. The former may be used by small retail businesses in fixed or variable values. The dynamic codes are Pix solution for companies, such as e-commerce, with creation of customized QR Codes for each sale.

Pix is already in operation. What to expect from it?

Every novelty brings opportunities and threats for different market players. The new system must promote a higher competition among payment means. Big techs, fintechs, digital banks and e-wallets celebrate its arrival. Purchasers, card carriers and payment processors may face problems with the deep changes caused by Pix. The traditional banks are also attentive to the opportunities and threats of loss of market share. According to Moody’s rating agency, they must lose up to 8% of the current revenue from operating fees.

With this, the Central Bank determined that Pix is mandatory to financial and payment institutions with more than 500 thousand active accounts. By launching date, 935 adhesion processes were opened and 677 institutions were approved by Central Bank. After agreement with the Ministry of Economy, government taxes and fees will also be paid through Pix.

Luiz Henrique Didier Jr., CEO of Bexs Banco, outlines a promising future for the Brazilian payment market: “Pix came to make a revolution in the method of payment and receipt for products and services, making it faster and more dynamic, but especially to strengthen the persons’ financial freedom, caused by the decentralized and democratic financial services”.